New 2025 trade data shows the U.S. imported 33 GW of solar modules and 21 GW of cells, even as domestic manufacturing expands. The U.S. solar market now runs on both growing local capacity and continued global supply, raising new questions about cost and competitiveness.

The U.S. Built a Solar Supply Chain. Imports Still Power the Market.

In November, we wrote that the United States had finally completed its solar supply chain. For the first time, every major component, from polysilicon to finished module, could be produced domestically.

That milestone mattered.

But the 2025 import data tells a more nuanced story.

What the 2025 Import Data Shows

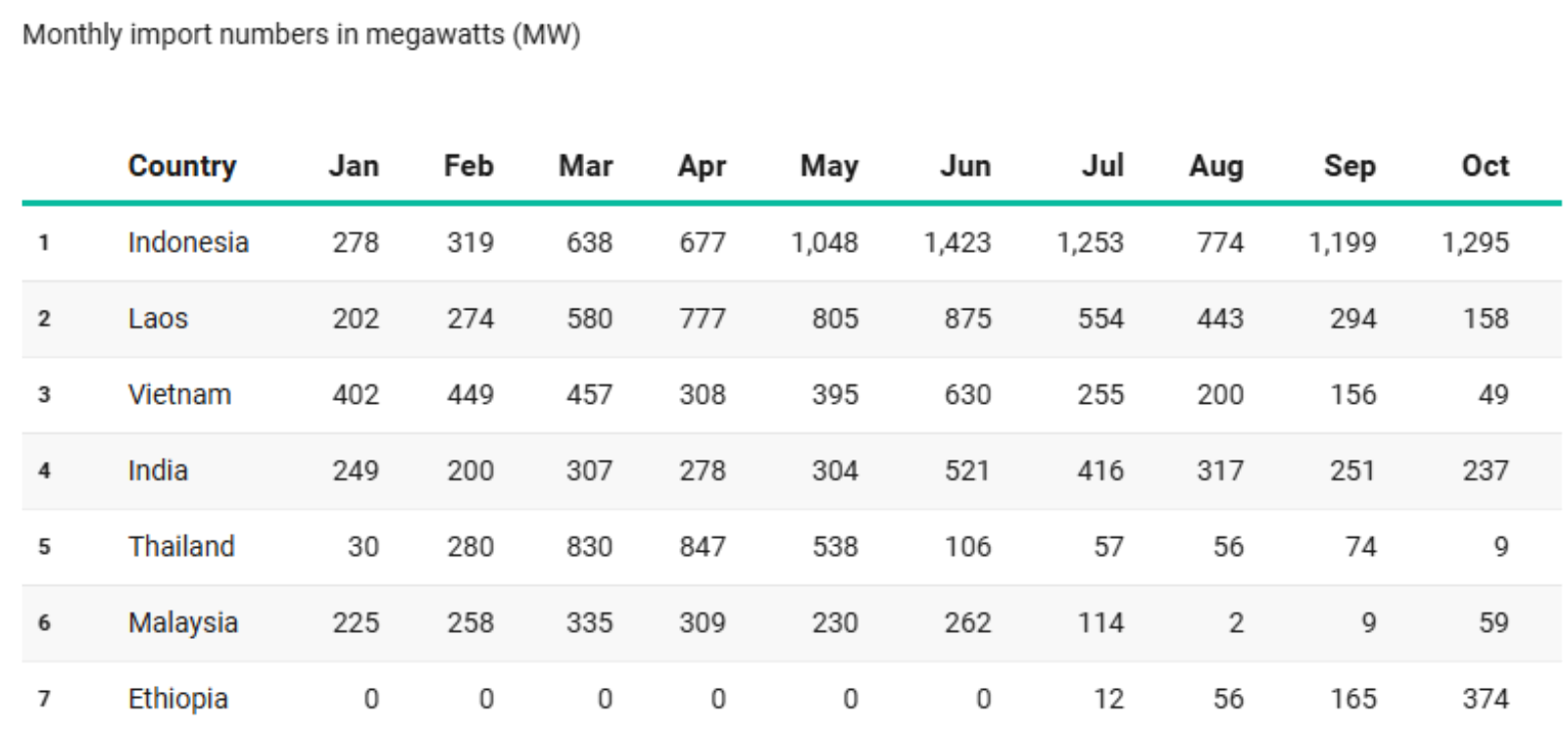

According to U.S. International Trade Commission data reviewed by Solar Power World, the U.S. imported 33 GW of silicon solar panels in 2025 and 21 GW of solar cells.

Most imported panels came from Indonesia, Laos, and India. All three are currently under investigation in an antidumping and countervailing duties case, where petitioners argue that producers benefited from unfair pricing and subsidies.

Cambodia’s role dropped sharply, falling from 4.5 GW in 2024 to just 3.3 MW in 2025.

New Exporters Emerging

Two new suppliers entered the picture in 2025. Ethiopia exported about 10.9 MW before December, and the Philippines exported about 29.74 MW. Then December alone saw 1,151 MW from Ethiopia and 545.3 MW from the Philippines.

On the cell side, most imports came from Indonesia and Laos, with South Korea also serving as a leading exporter.

The supply map is shifting.

The Structural Imbalance

Here is the underlying dynamic.

The U.S. now has roughly 50 to 60 GW of module assembly capacity, depending on the source. Domestic solar cell production, however, remains below 5 GW.

That gap explains the import volumes.

Assembly vs. Cell Production

Module assembly capacity has scaled quickly due to federal incentives and industrial policy. Cell manufacturing has not yet caught up at the same pace. As a result, even as the U.S. assembles more panels domestically, it still relies heavily on imported cells and finished modules to meet demand.

Domestic manufacturing is expanding fast.

But imports are still carrying a significant share of supply.

Jobs, Security, and Cost

This dual system is not automatically a weakness.

Imported panels are often cheaper and help control project costs. That affects developers, utilities, and ultimately customers. Lower hardware costs can accelerate deployment.

At the same time, domestic factories support job creation, supply chain resilience, and reduced geopolitical risk.

Right now, the U.S. solar market runs on both forces: domestic industrial growth and global supply.

The Strategic Question

The challenge ahead is not simply replacing imports. It is expanding local manufacturing in a way that preserves cost competitiveness.

If domestic capacity grows too slowly, reliance on imports continues. If trade barriers raise prices too sharply, deployment could slow.

The next phase of U.S. solar policy will hinge on balancing scale, affordability, and supply security.

The supply chain may be technically complete.

But the market remains globally interconnected.

Ready to Discuss Your Project?

Get your instant estimate or talk to our team about your legacy solar project.